Many contractors confuse the word "salary" with the word "profit." There is a difference. The Merriam-Webster dictionary defines profit as: “1) a valuable return, 2) the excess of returns over expenditure in a transaction or series of transactions especially: the excess of the selling price of goods over their cost, 3) the compensation accruing to entrepreneurs for the assumption of risk in business enterprise as distinguished from wages or rent.” It defines salary as fixed compensation paid regularly for services.

Salary is the compensation paid to employees of a business for the services those employees deliver to the company. Salary is a legitimate business expense. If you manage your business, you are an employee of your business. Therefore, the cost of your salary as manager and technician must be included in your cost structure if you want to develop properly profitable selling prices.

I know if you came to work for me and managed my business, you would expect to be paid for your service to my business. In your own business, if you neglect to include a salary for yourself when calculating your costs, your selling prices will not allow you to receive the reward you deserve for the risks you take serving the public.

Salary and salary-related expenses, including that of business owners who manage the business, are business expenses similar to business insurance, vehicular costs, rent and such. Profit is the money left over after all business expenses are paid.

Those investing in a business are doing so in hopes of receiving a return on their investment greater than their original investment. If you invested $1,000 in a project and received $1,100 in return, your profit would be $100. The initial $1,000 was meant to pay for all legitimate business expenses, one of which is the salary expense. The $100 above the $1,000 is profit.

However, many contractors look at the amount of money they bring in, deduct the amount of money for bills they incur running their business, inclusive of all employee salary expenses except for their own salary expenses, and then claim the remaining amount of money, if any, as profit.

But let’s say your management salary cost for the project is $100 and you don’t include it in your cost estimate. You would then erroneously calculate your cost to be $900. If you added $100, your selling price for the project would be $1,000. Is the added $100 profit or salary?

If you see it as profit, you received no pay for your management services to your business. If you see it as salary, you received no profit. The only way you can have it both ways is if you realize that salary and profit are two different issues to address when developing selling prices. Simply put — salary is not profit and profit is not salary.

Maximized profit

I’ve heard contractors who call me for business coaching claim they are profitable. The fact that they are calling me for help suggests they are not happy with the amount of profit, if any, they are receiving as a return on their investment in their business.

The reason they aren’t satisfied with the profit is that it isn’t maximized profit — if profitable at all. One of the reasons it isn’t maximized profit is that they do not include their salary and salary-related expenses when identifying and calculating their business costs. This miscalculation leads them to undercharge for their services. In turn, the profitability of their businesses suffers and, instead of profits, they may encounter losses. Wrong numbers produce wrong results.

When I bring up this fact, they tell me their accountant said the money they receive is a profit. When people speak, it is essential to understand from where their words emanate. Accountants look at your financial situation from a perspective of tax implications. If your tax liability is legitimately less by claiming the revenue you receive from your business is a profit rather than a salary, the accountant is doing his job in your best interests.

However, this does not relieve you of the responsibility of including your salary and salary-related expenses when identifying and calculating your actual operational costs so you can correctly develop properly profitable selling prices for your services.

Let’s look at the overhead costs of a one-person PHC service contracting business operated from the kitchen table. That overhead cost is minimally $54 in hourly overhead expenses for each of his available saleable tech hours if all open tech hours are sold all the time.

Note I use the word minimally. I’ve only included vehicular, health, utility, office supplies/equipment, accounting, customer relations, bad debt and tool expenses at the minimum cost that would be incurred. I believe that overhead costs to be between $75 and $150, dependent upon geographic location. And, to that range, tech salary expenses must still be added.

If the contractor didn’t include his salary and salary-related expenses in price calculations, his selling prices would be grossly undercharged. A tech hour of service time at $54 and a 50 percent profit margin would be sold at $108 ($54 divided by 50 percent).

You might be thinking a 50 percent profit margin is insane. Not really. No PHC service contractor sells all available tech hours all the time. During normal economic times, PHC service contractors sell about 70 percent of their available tech hours. To break even at 70 percent of open tech hours sold, you would need a 30 percent profit margin on your labor and overhead costs based on selling all your hours all the time. But you didn’t go into business to break even.

Profit margins and selling prices

Profit margins are that percent of the selling price not allocated to labor, overhead and material expenses. To arrive at a profit margin, you would subtract the desired profit margin from 100 percent, then divide the cost of labor, overhead and material by the difference. For example, a 100 percent less 50 percent desired profit margin equals 50 percent margin divisor. Then divide the cost of labor, overhead and material by the margin divisor of 50 percent.

If you want a 40 percent profit margin, divide by a 60 percent margin divisor. A 30 percent profit margin requires a 70 percent margin divisor.

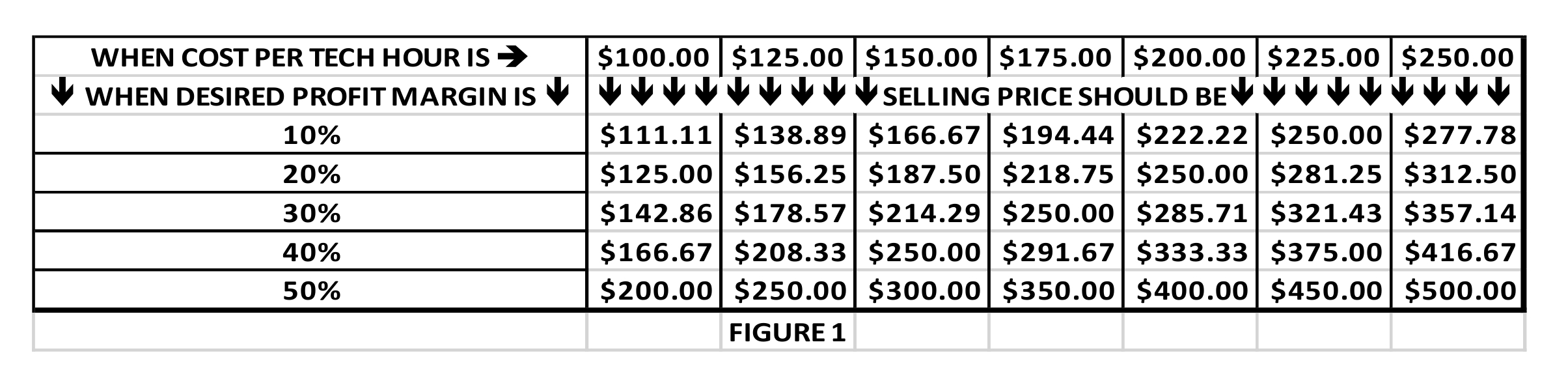

As I have stated, wrong numbers produce wrong results. The reality is the true minimum labor and overhead cost for one qualified service tech and a properly equipped service vehicle in the United States ranges between $100/tech hour and $250/tech hour if all hours are sold all the time.

Figure 1 shows where the example one-person business selling price would be at different labor/overhead cost levels and profit margins.

In each instance, the selling price is higher than the $108 the business owner would charge by not including his salary and related salary expenses.

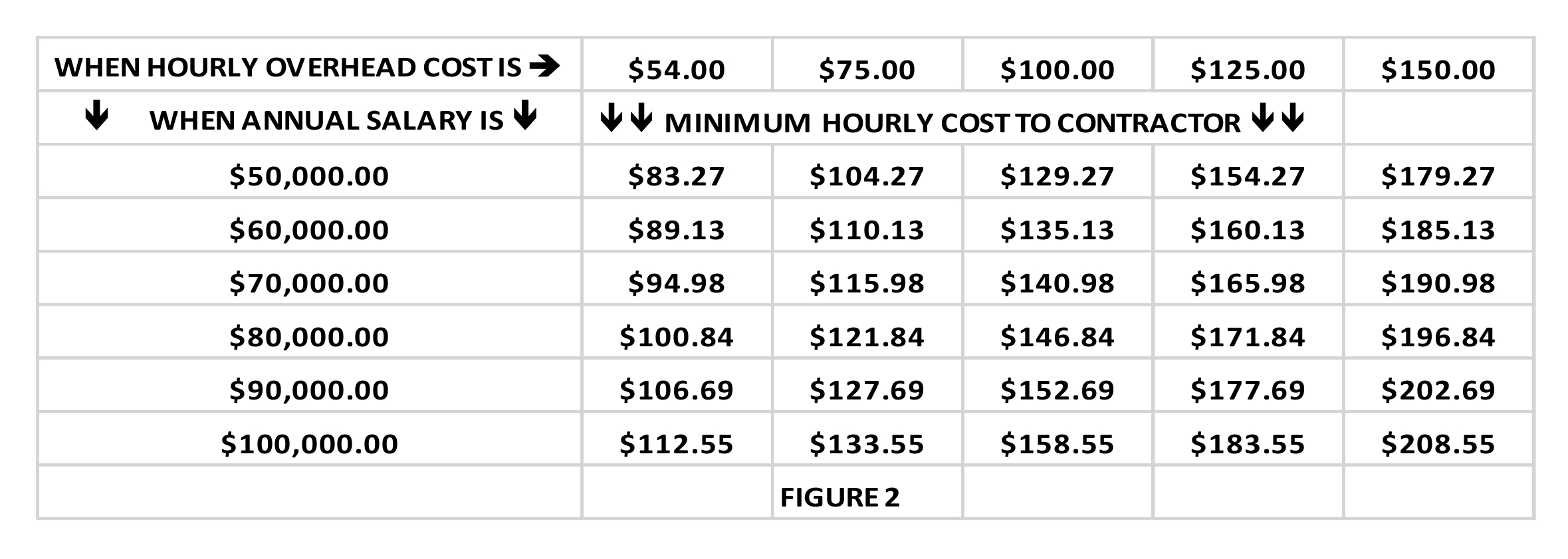

Figure 2 shows the minimum cost the one-person business owner would incur if he included his salary and salary-related expenses at different salary levels and if he sold all available tech hours all the time.

As you can see, at the minimum hourly overhead cost of $54, the labor/overhead cost is $83.27 if all available tech hours are sold. But at only 90 percent of hours sold, that $83.27 rises to $92.52. At 80 percent of possible hours sold, the $83.27 rises to $104.09. And at only 70 percent of hours sold, that $83.27 rises to $118.96.

At the overhead cost range of $75 to $150, only once at $104.27 does the cost to the contractor fall below the $108 selling price. But since no contractor sells all available tech hours all the time, even the cost would, in reality, be higher. If he sold 90 percent of available hours, the cost per tech hour would rise to be $115.86.

Even if you don’t grasp the numbers, you should grasp this logic:

- If you wouldn’t work for someone else without a salary, don’t work for yourself without including a salary expense for yourself in your selling prices.

- Profit is the reward you receive for the risks you take delivering excellence to consumers.

- To attain a profit, you must correctly calculate the numbers for all business expenses and apply a profit margin that can get you where you want to go.

- Wrong numbers produce wrong results.

- Your salary is a legitimate business expense.

If you need help, I’m as close as your phone.