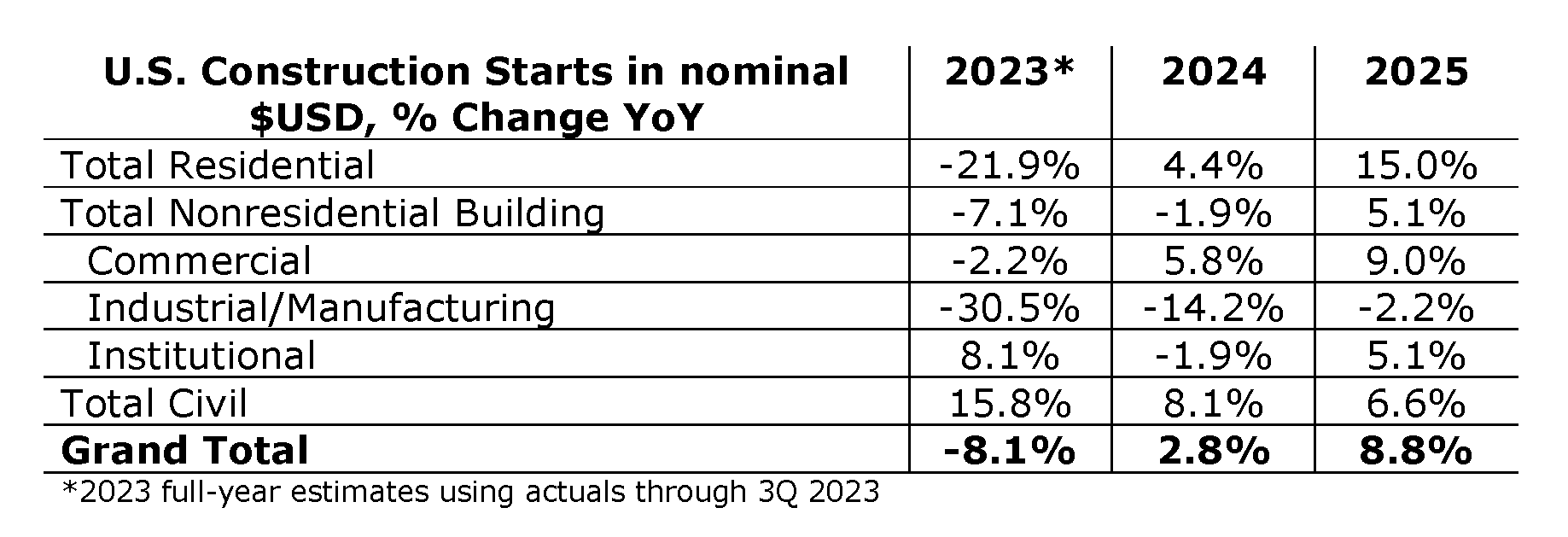

In ConstructConnect’s 2023 outlook, we correctly identified several factors that impacted the construction and trades industries. Our concern regarding single-family housing construction and our more prosaic outlook for multifamily construction proved generally on-target.

U.S. single-family housing starts fell early in 2023 to approximately 800,000 units annually, marking a four-year low when excluding COVID-19’s brief but exceptional impact on 2020 results. Multifamily construction performed relatively better, with permits continuing to ride the wave of strong demand. Dissimilar to the single-family market, multifamily permit levels through the third quarter of 2023 remained well above pre-pandemic levels.

In our prior outlook, we also anticipated double-digit construction start growth within the community, military and retail verticals. Per the latest available data through September 2023, community spending had increased by 14%, retail came in below expectations with 4% growth, and military spending was up by a hefty 59%.

Furthermore, we called out excessive levels of inventories-to-sales and encouraged firms to reduce excessive inventories, especially at a time when construction material prices, in general, were falling.

2024 Category Outlook

• Nonresidential:

ConstructConnect’s construction starts outlook in 2024 and 2025 is generally positive, coming off a difficult 2023. In the aggregate, the sector is expected to achieve mid-single-digit growth through 2025. However, category-specific outlooks vary widely based on factors specific to each.

Among nonresidential categories, transportation terminals, hotels and motels, shopping and retail, and warehouses are all expected to grow in excess of 20% by year-end 2025. Conversely, amusement parks, government offices and sports stadiums are not expected to experience meaningful growth during the same period.

• Housing:

The subdued single-family housing market of 2023 stemmed from events in 2022 and earlier. Starting at 2.7% in early 2021, the 30-year mortgage rate started 2023 at 6% and would eventually reach a two-decade high of 7.8% by October. Further, new single-family home prices surged 50% over the four years ending December 2022. Collectively these factors clipped demand beginning in 2022 and would carry over well into 2023.

The subdued single-family housing market of 2023 stemmed from events in 2022 and earlier. Starting at 2.7% in early 2021, the 30-year mortgage rate started 2023 at 6% and would eventually reach a two-decade high of 7.8% by October. Further, new single-family home prices surged 50% over the four years ending December 2022. Collectively these factors clipped demand beginning in 2022 and would carry over well into 2023.

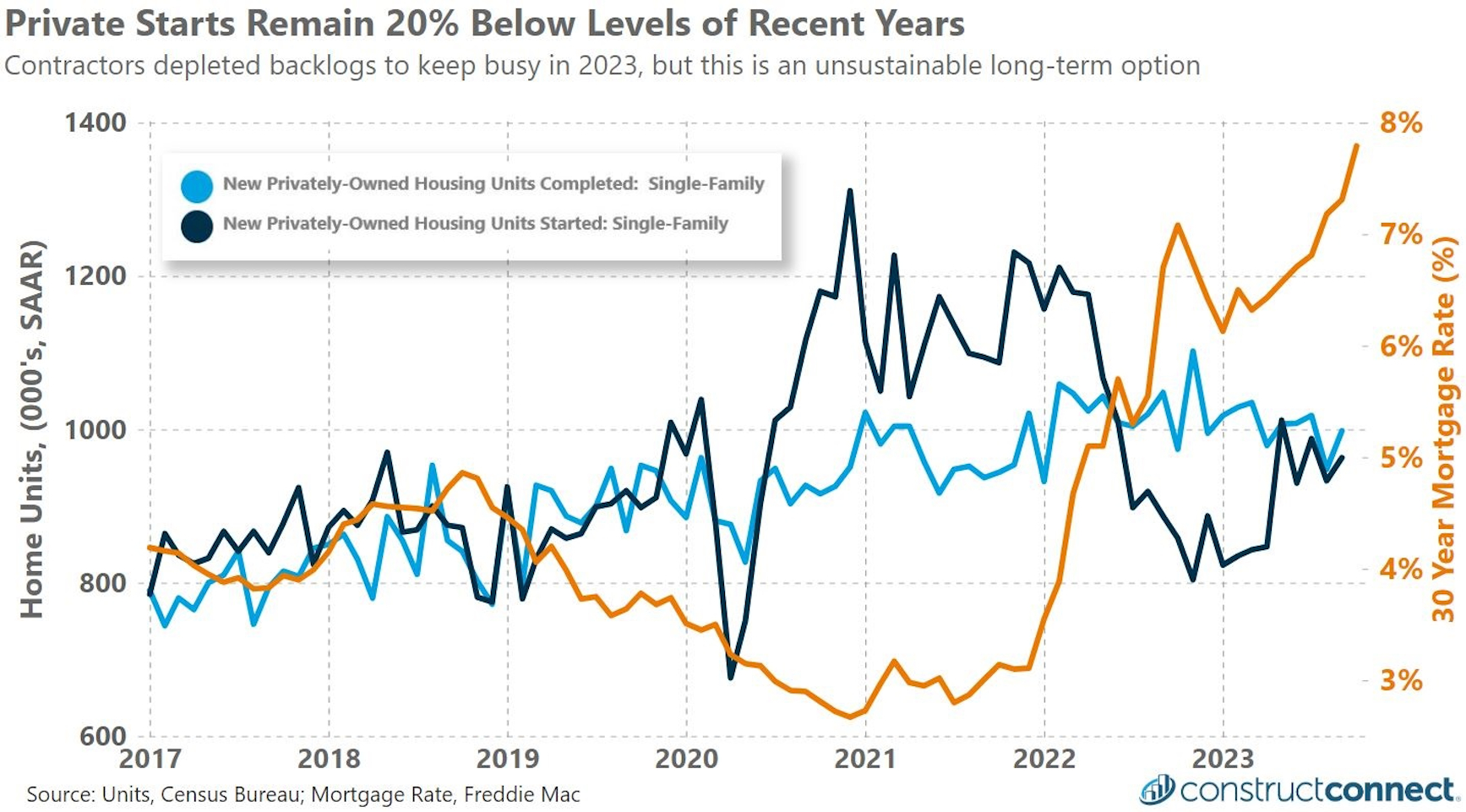

Contractors, unable to adapt to these swiftly changing market forces, faced an excess capacity problem, completing five homes for every four started. However, by late 2023, the oversupply issue had been largely resolved as starts and completions approached parity. Reaching this equilibrium in the third quarter however required a 25% decline in new starts activity compared to just 18-months ago (see Figure 1).

Housing affordability (a function of median home prices, typical family incomes and mortgage rates) will play a key role in the future health of the residential market. In 2023, the National Association of Realtors Housing Affordability Index set an all-time low based on its findings that the typical family’s income was nearly $9,000 below what is required to afford a median-priced home in the United States.

Such dynamics have been a tailwind for the construction of rental housing and an underlying reason why multifamily construction is expected to perform modestly better than single-family construction in 2024 (see Figure 2). However, with so many contractors attempting to take advantage of recent conditions, the supply of new housing for rental purposes could result in a supply glut, especially in popular geographies.

The recent pace of rental housing construction was 50% above pre-pandemic levels and double that of forecasted long-run demand, according to the National Apartment Association and the National Multi-family Housing Council.

2024 Labor and Financial Trends

• Labor market:

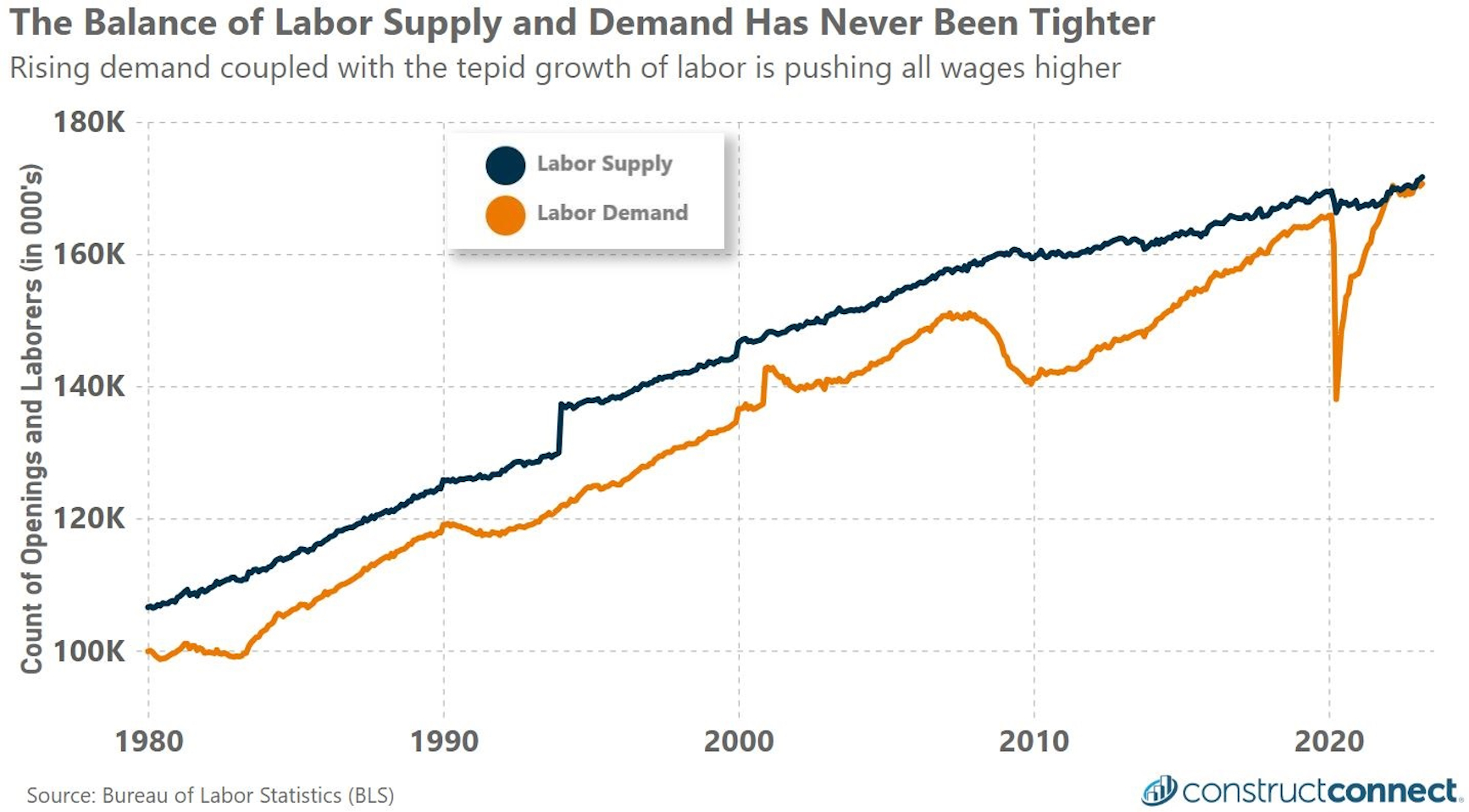

The challenges facing today’s construction workforce are not the result of a single problem, but rather multiple latent problems whose consequences were merely sped to their tipping point by COVID-19. In past decades, extra laborers have always been available to fill fluctuating levels of job openings. However, between 1980 and 2019, that pool or “gap” of excess laborers slowly shrank from more than 11 million to 4 million (see Figure 3).

As such, beginning in 2020, when the U.S. government instituted extraordinary measures, including providing stimulus checks to spur consumption and visa restrictions to reduce immigrant levels, that pool of excess workers quickly collapsed and job openings for the first time in generations exceeded available workers.

Barring either a recession that reduces labor demand or a surge in immigration, there are no quick fixes to reinflate today’s labor supply gap. As recently as September 2023, there were more unfilled construction positions than unemployed people with previous construction experience. Given such conditions, retaining and recruiting qualified labor will remain a significant problem in 2024.

The problem will be difficult for the general construction industry at large, but especially so for the specialty construction industry (see Figure 4). In the previous four years, the number of nonresidential specialty trades laborers grew by less than 1%, while the number of nonresidential construction laborers increased by a similarly paltry 1.6%.

Such limited gains in specialized workforces, when compared to the industry’s significant growth in recent years, suggest that 2024 is almost certain to see a continuation of the battle for labor amongst businesses.

This ongoing battle will place a floor under wage growth in 2024 and further put the onus of training new recruits on the shoulders of managers. Within the general construction industry, annualized pay growth will remain elevated at around 3.5% to 5%, but down from the 5.9% climax witnessed in late 2022.

The general deceleration in recent construction wage growth may be irrelevant to employers of nonresidential and specialty trades workers given the tepid growth in their numbers post pandemic and exceptionally strong demand.

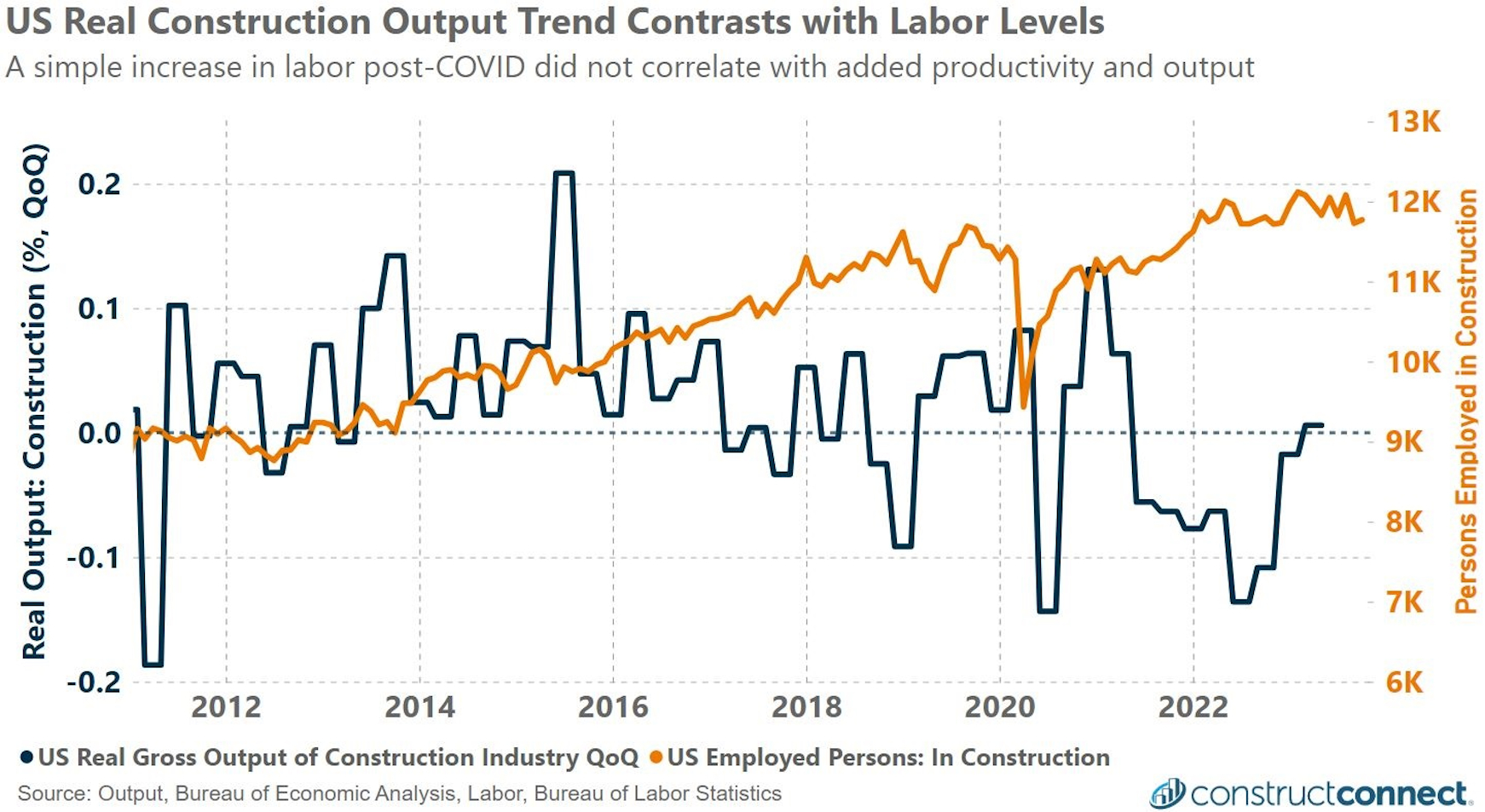

Even if a future recession were to help reinflate the labor gap, it would not resolve the national decline in productivity per laborer (see Figure 5). One of COVID-19’s most devastating impacts on the labor force was that it sped the loss of workers with decades of expertise. Their former positions have since been filled with much less experienced replacements, assuming they can be filled at all.

The result is that businesses continue to grapple with a structurally different labor pool that is not only short of workers but particularly short on experience. As a result, business owners who hope to set themselves apart from their competitors should consider making extraordinary investments in their employee training and development programs in 2024 and beyond.

• Construction Labor Legislation:

A slew of new and forthcoming legislation from all levels of government will significantly impact costs in 2024 and thereafter. In February 2022, by executive order, Project Labor Agreements (PLAs) were mandated for all federally funded projects with contract values above $35 million.

These individual project agreements with organized labor have been estimated to increase labor costs for large projects by between 12% and 20%, according to the Association of Building Contractors (ABC), along with disadvantaging local and small nonunion businesses. Given the substantial number of federal construction projects that will be affected by the institution of PLAs, contractors can expect to see increased labor costs across the board and nonunion firms effectively excluded from the bidding process.

In 2023, the Department of Labor overhauled the Davis-Bacon Act, which calculates prevailing wages on federally funded projects. The revised laws will reduce the standard by which prevailing wage rates are determined. This effectively allows rigid government pay tables to override the wages that would otherwise be determined by efficient market forces. It will impact 63% of all government construction projects, amounting to hundreds of billions of dollars of work, according to the ABC.

Additional layers of localized labor rules will further add to the cost and complexity of managing construction costs; for example, the growing implementation of state laws offering heat protection standards mandating short breaks for workers every few hours on days when the outside temperature exceeds a certain level.

Ultimately, the combination of new and existing legislation at all levels of government creates hard-to-establish net effects that can quickly drive up labor costs while simultaneously decreasing productivity.

• Inflation and interest rates:

Although inflation and interest rates are separate entities, the Federal Reserve’s strategy in recent decades has been to directionally move interest rates with inflation until such actions achieve a steady inflation rate of 2%. The Fed’s unprecedented aggressiveness in raising interest rates beginning in early 2022 was a drastic reactionary response to inflation rates, which rose from a benign 1.2% in 2021 to a multidecade high of over 7% by year’s end.

However, this strategy has direct and explicit consequences for the private sector, as rising interest rates make the cost of funding operations and investments with borrowed capital more expensive, ultimately lowering returns on investments.

Presently, the Fed continues to signal that it intends to keep interest rates elevated well into 2025. As such, businesses should not attempt to “wait out” today’s elevated rate environment, but rather adjust and optimize their operations to this higher rate environment. Business owners must be cognizant that rate changes have not only immediate, but also powerful delayed effects, which have yet to be fully understood on the economy.

Among the most concerning delayed effects is refinancing existing debt as it comes due in the coming quarters. Within the construction sector specifically, great concern remains that commercial real estate (CRE) prices have yet to adjust to today’s higher rate environment. In 2024 and 2025, nearly $1.5 trillion of CRE debt will come due, which must be refinanced at today’s higher rates.

For the 25% of this debt that is tied to office buildings, higher mortgage payments combined with entrenched work-from-home trends could result in rising CRE office loan defaults and bank repossessions. In several instances during the second half of 2023, distressed office buildings sold for approximately 65% of their original values.

Thus, the forthcoming wave of refinancing, coupled with the Fed’s intention to hold rates higher for longer, presents a strong reason for developers and contractors to tread cautiously and deploy capital conservatively in the near term.

The immediate impact of higher rates has already manifested itself in the short-term debt and revolving credit markets, exposing financially weaker customers and partners, as evidenced by the five-fold surge in the value of delinquent commercial and industrial loans which climaxed in early 2023 (see Figure 6). Although the total value of delinquent loans as of late 2023 had fallen from that peak, it remains three times greater than during the same period in 2021.

Looking ahead, firms should use strong discretion when determining to whom they will extend credit and carefully manage their total accounts receivable so it does not become an existential threat to their company in the event of a rising nonpayment environment.

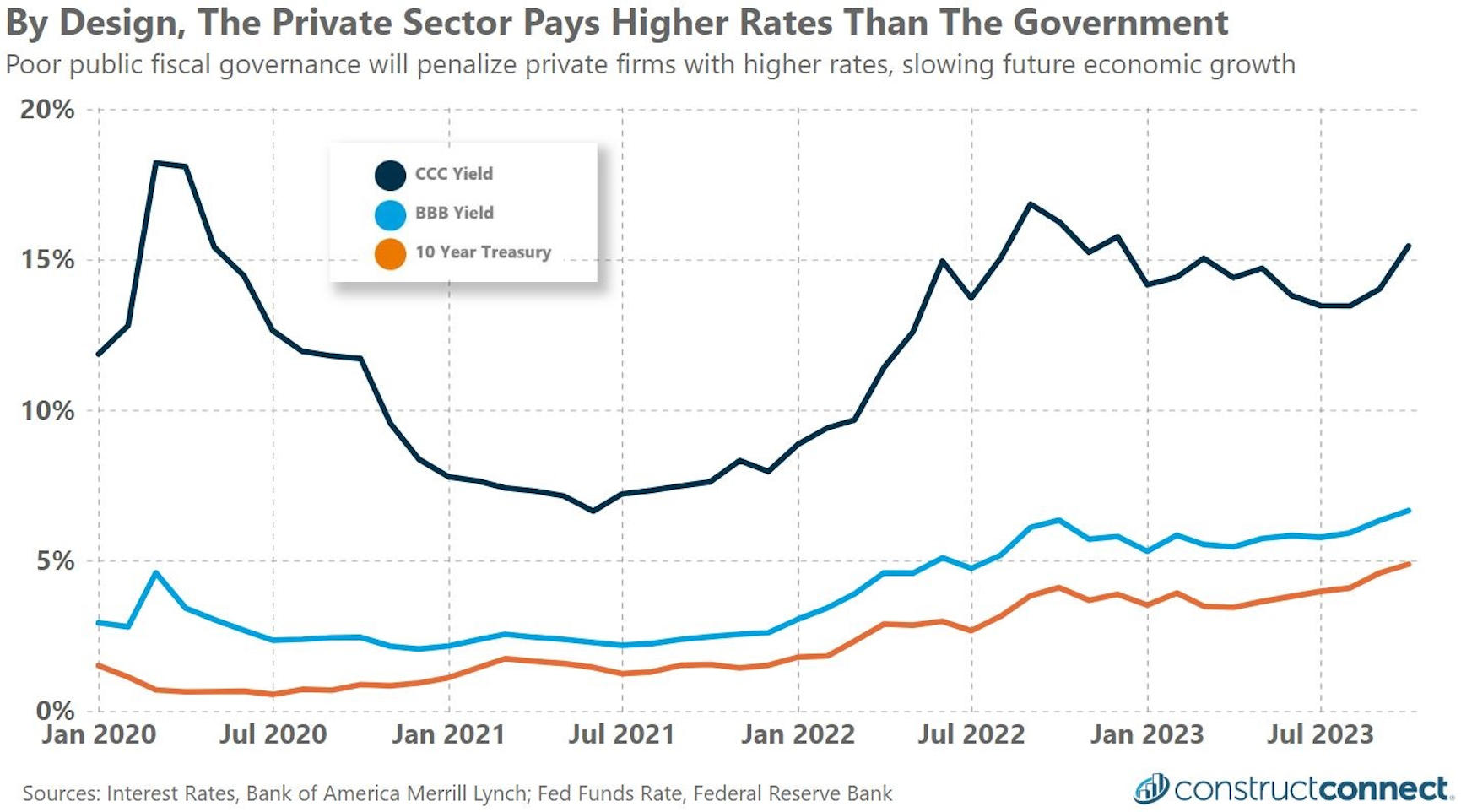

The U.S. government’s unsustainable fiscal policy also has ramifications for the construction industry. Decades of past deficit spending with no clear path for repayment has elevated the risk of holding treasury debt, resulting in lenders recently demanding higher rates of return to hold government debt. Private industry credit rates, established by banks adding a premium to the rate paid on government debt, now include this penalty on private debt as well (see Figure 7).

The government’s debt problem is also a risk to future public infrastructure and public-private investments. Unless substantial progress is made to manage the public debt, publicly funded construction projects will compete with schools and the defense department over a vastly smaller pool of discretionary spending dollars.

• Supply chains:

Supply chains began normalizing in 2023 after more than two years of historic disruptions to the industry. The investments in equipment and labor made during those tumultuous years ultimately resulted in a glut of capacity that both lowered shipping costs and improved delivery times beginning in late 2022 and lasting through 2023.

Current trucking rates continue to reflect the transportation market’s oversupply problem. Trucking spot prices fell by more than 30% between the start and end of 2023. Similarly, container freight shipping rates between China and western U.S. ports declined rapidly during 2022, allowing for 2023 prices to return to pre-COVID rates of as low as $1,700 per container.

As the transportation market continues to resolve its remaining overcapacity problems, the downward pressure exerted by excess capacity will diminish, giving way to other pricing dynamics. Surveys of transportation CEOs in 2023’s fourth quarter noted their substantial concern over expected lackluster demand for transport services in 2024 and not merely the industry’s remaining overcapacity.

Depressed transportation costs, the generally good availability of construction materials, and stable, if not in some instances falling material prices, suggest that all the necessary dynamics are in place for business owners to save costs by pursuing just-in-time and similar supply chain strategies. This will be especially true of firms purchasing inventory using credit.

During the height of COVID-19, many copper products saw strong double-digit price increases and poor availability. This led many rational firms to hoard inventory when and wherever possible. Single-digit interest rates made buying excess supplies on credit an obvious choice when many materials were experiencing 50% or greater price increases.

Today’s situation could not be more different, with copper product price expectations to remain muted and interest rates expected to remain elevated into early 2025. This inversion in the movement of product prices and interest rates will make 2024 a particularly well-suited year for inventory minimization strategies.

Applying These Insights in 2024

The fact that the economy seems to have not only avoided a recession during 2023 but, in the third quarter, reported its strongest gross domestic product growth in several years, seems to defy the odds along with modern economic theory. Sequential quarters of eroding real incomes, excessively priced assets, rising interest rates and two years of depressed consumer sentiment readings have all been historically reliable indicators of pending recessions.

The present day’s unique combination of events leaves one to believe that the jobs market is sustaining a disproportionate share of the economy and that any weakness in future readings could be a harbinger of a recession.

Current data and trends suggest that 2024 will be one of generally stable material prices and slowly decelerating wages, but also high interest rates and tight-fisted creditors. Given this outlook, the most profitable firms in 2024 will likely be those willing to return to the kinds of supply chain practices that closely follow customer demand movements and minimize inventory and carrying costs.

As the balance of labor supply and demand further moderates throughout the year, employers may see an increase in their labor negotiating power; however, this may be at risk due to changes in 2023’s labor compensation law. While 2023 saw laborers achieve record-setting compensation gains, this exceptional opportunity appears to be in the early stages of decline as both construction job openings and hourly wage growth have descended from those highs.

Importantly, recent data indicates that switching jobs no longer pays the substantial premium it once did. Additional decelerating wage growth through the first half of 2024 may give employers a stronger hand at the negotiating table later in the year.

Lastly, adjust your business practices as necessary for an extended period of elevated interest rates. A rising rate environment may not be fateful to your business, but it could be to those with accounts payable to your business. Managing operations with an eye to cash-flow generation and debt minimization, along with having diversified streams of revenue across multiple construction verticals, will help safeguard your 2024 success.

Michael Guckes, senior economist at ConstructConnect, has more than 20 years of experience in economics, including eight years in civil construction and six years in manufacturing. Guckes joined ConstructConnect’s economics team in 2022, shifting his focus to the nonresidential and civil construction markets. He received his BA in economics and political science from Kenyon College and his MBA from The Ohio State University.