It is undisputed that the COVID-19 pandemic generated unprecedented manufacturing and construction industry challenges in its wake. In a single moment, the operation of a wide range of companies was effectively shuttered while government stimulus and restrictive regulations gave consumers strong incentive to purchase durable goods, in part because purchases of services were highly restricted.

The immediate effect of these forces was an imbalance in the supply and demand for material products. The construction industry scrambled along with its upstream suppliers and products manufacturers to quickly find enough resources and logistics capacity to meet surging demand.

For much of the two years starting in early 2020, the greatest impediment to growth for many in the construction and trades industry was the limited availability of materials and labor. The word “hoarding” was ubiquitously used by many business leaders as a reasonable solution to their unprecedented situation.

It would not be until inflation began sapping consumer’s spending power in 2022 that the economy would begin a phase change toward slowing economic expansion. By mid-June, consumer confidence readings had fallen to an all-time low, an explicit signal of waning demand. Souring consumer purchases of durable goods quickly led to overstocking along the supply chain.

These events make plain the fact that the U.S. economy was in a cyclical transition during 2022. As such, 2023 will see new and distinctive challenges for business leaders and necessitate the implementation of very different operational and business strategies that have little resemblance to the plans of the last two years.

In short, industry leaders should consider the following in the development of their 2023 plans:

The substantial change occurring within residential construction;

The prospects of select nonresidential opportunities;

The importance of right-sizing inventory at a precarious stage in the economic cycle along with the risks of holding excessive levels of devaluing inventory.

Residential Market Opportunities Will Look Very Different in 2023

Between February 2020 and June 2022, the median home price surged 54% to an all-time high of $420,900. This rapid change was, in part, thanks to low interest rates and a shift in housing preference out of COVID-restricted cities and toward relatively more open suburbs.

Rapid home price growth greatly exceeded the modest 5.7% rise in median incomes over the same time. As a result, the median home price to annual income ratio soared from 3.3x to a lofty 4.8x by the end of 2021.

This would not last long, however, as mortgage rates doubled from around 3% at the end of 2021 to more than 7% a year later. For many prospective homeowners, this created an insurmountable cash flow problem. Buying a same-price house at the end of 2022 as compared to a year earlier meant carrying a monthly mortgage payment that was many hundreds of dollars greater, a feat that for many was not possible, especially when inflation at a 40-year high was already straining budgets.

These changes to the market resulted in the sharp slowing of single-family housing demand. Housing permit data through the first three quarters of 2022 fell by 27% to mid-2019 levels. Even more alarming, mortgage originations by dollar value fell more than 50% during the same period. The last time a decline of this magnitude occurred was in the lead up to the Great Recession.

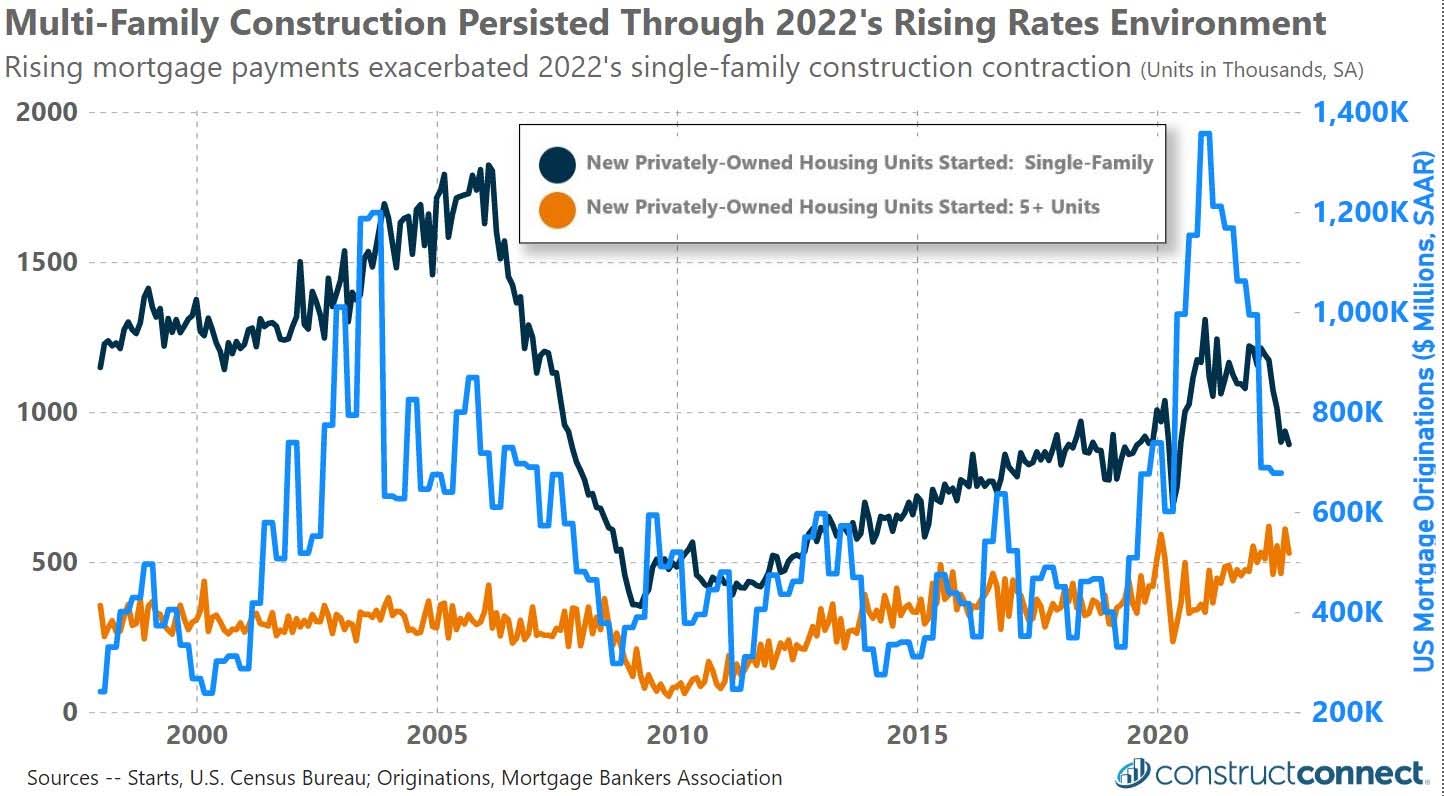

Thankfully, the prospects for multifamily construction as of October 2022 remained strong, with starts sustaining their upward trend initiated during the first half of 2020. Unlike the financial dynamics which have slowed owner-occupant home construction, soaring rental rates have offset rising construction and financing costs for lessors and apartment developers.

Demand for multifamily construction will benefit into the future thanks to three demographic fundamentals of the millennial generation. First, they are the largest generation by population count at 78 million. Second, ranging in age from 27 to 42 years old, many of them have yet to form new households and the necessary housing for this next stage of their lives.

Lastly, data from the Federal Reserve as of 2022 indicated that millennials possess far less wealth at this stage in their lives than previous generations when adjusted for age. For these reasons, multifamily housing is and will remain an attractive option for this generation.

According to the U.S. Census Bureau, U.S. real estate, rental and leasing sector total revenues increased by 52% in the two-year period ending June 2022. Such spectacular revenue growth has more than offset the higher interest rates that real estate investors are paying on borrowed capital (see Figure 1).

Select Nonresidential Market Opportunities in 2023 and Beyond

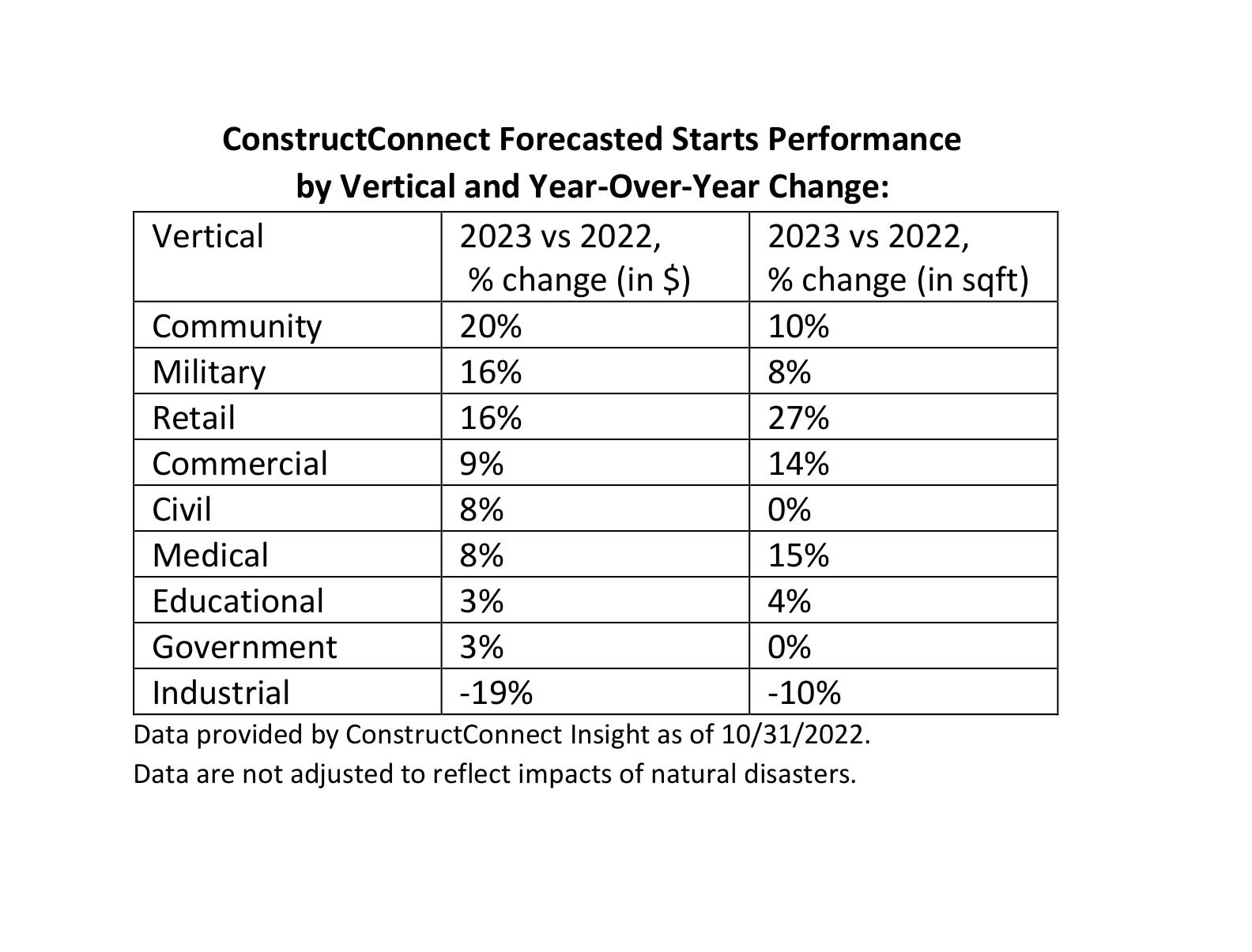

The performance of other segments of the construction industry are available through proprietary construction databases such as ConstructConnect’s Insight service, which monitors more than 60% of all U.S. construction projects, in addition to Canadian construction data. Our 2023 forecasts by market vertical expect double-digit growth in dollar terms for the community, military and retail verticals.

Also, strong single-digit growth is expected in the commercial, civil and medical construction markets. Furthermore, forecasts measured in square feet provide an inflation-adjusted outlook for each vertical market. Such nondollar forecasts provide a more reliable outlook of construction demand during periods of high inflation (see Figure 2).

Across all verticals, another important trend for business leaders to consider is the growing number of “mega” projects, defined as projects more than $1 billion in size. As recently as 2019, mega projects constituted approximately 10% of all nonresidential construction; in contrast, that figure during the third quarter of 2022 neared 30%.

There are many reasons for the rise of mega projects; however, among the top reasons is to transition America’s supply chains away from being heavily globalized and, thus, dependent on the actions and decisions of foreign leaders. The intention here is that by narrowing the geographic footprint of supply chains, the fate and future of America’s economy will rest more with the decision-making of North American leaders and less with those of more distant foreign leaders.

For example, the creation of new multibillion-dollar computer chip foundries and electric vehicle and associated battery plants in the United States will reduce America’s dependency on Asian nations for critical components that are necessary and essential for both America’s largest and most high-tech industries — and American consumers way of life.

It is for these reasons that ConstructConnect sees strong “pockets” of opportunity by select industries and geographies. Finding these prospects requires firms to not only work harder, but smarter.

Another major source of mega projects will come from the fracturing of what was once a single global energy market. Regardless of the outcome in Ukraine, what has been made clear is the ability of geopolitical actors to threaten other nation’s energy security.

One response to such acts has been the March 2022 agreement designed to increase liquified natural gas (LNG) exports from the United States to the European Union, starting with a pledge to export 15 billion cubic meters (bcm) of LNG the first year. Annual commitments would increase to 50 bcm by 2030. Such a commitment, if fully enacted, could require a significant expansion of the U.S. energy market’s infrastructure.

For context, 50 bcm converts to 1.7 trillion cubic feet (tcf) of natural gas, an amount which represents a very sizable portion of the available U.S. working gas stored underground throughout the year. U.S. working gas stored underground fluctuates seasonally, with volumes oscillating in recent years between a high of 3.9 tcf going into the winter and a low of 1.5 tcf by the start of spring.

As America’s role as energy provider to the Western Hemisphere grows, so will demand and prices until supplies can better match this new demand. U.S. spot prices August 2022 at $8.93/million BTU were more than double February’s price of $4.46/million BTU.

These prices pale in comparison to European import prices, which have soared from more than $6/million BTU in early 2022 to between $30/million BTU and $70/million BTU. (Spot prices provided from the Energy Inflation Association and the New York Mercantile Exchange.)

Such price increases are nearly certain to speed along the construction of the 14 LNG projects which have already been federally approved, but not yet built (http://bit.ly/3OMfiq4). Associated infrastructure needs for the exploration, extraction and transportation of all this gas will add another layer of construction demand on top of existing energy infrastructure plans and, in particular, those for alternative energy.

Right-Sizing Inventories

The last two years of supply chain disruptions were unusually challenging for supply chain managers, resulting in the frequent hoarding of materials among manufacturers and contractors. Just-in-time inventory management gave way to many manufacturers and contractors at times buying all available inventory, even if there was not an immediate plan for its use.

Beyond simply increasing inventories, business owners expanded their supply chain networks with new suppliers and distributors, along with using software to make better informed supply chain and purchasing decisions, according to a survey conducted by ConstructConnect in early 2022. We expect these later changes to be enduring, with the net affect being a more competitive market for upstream producers and distributors.

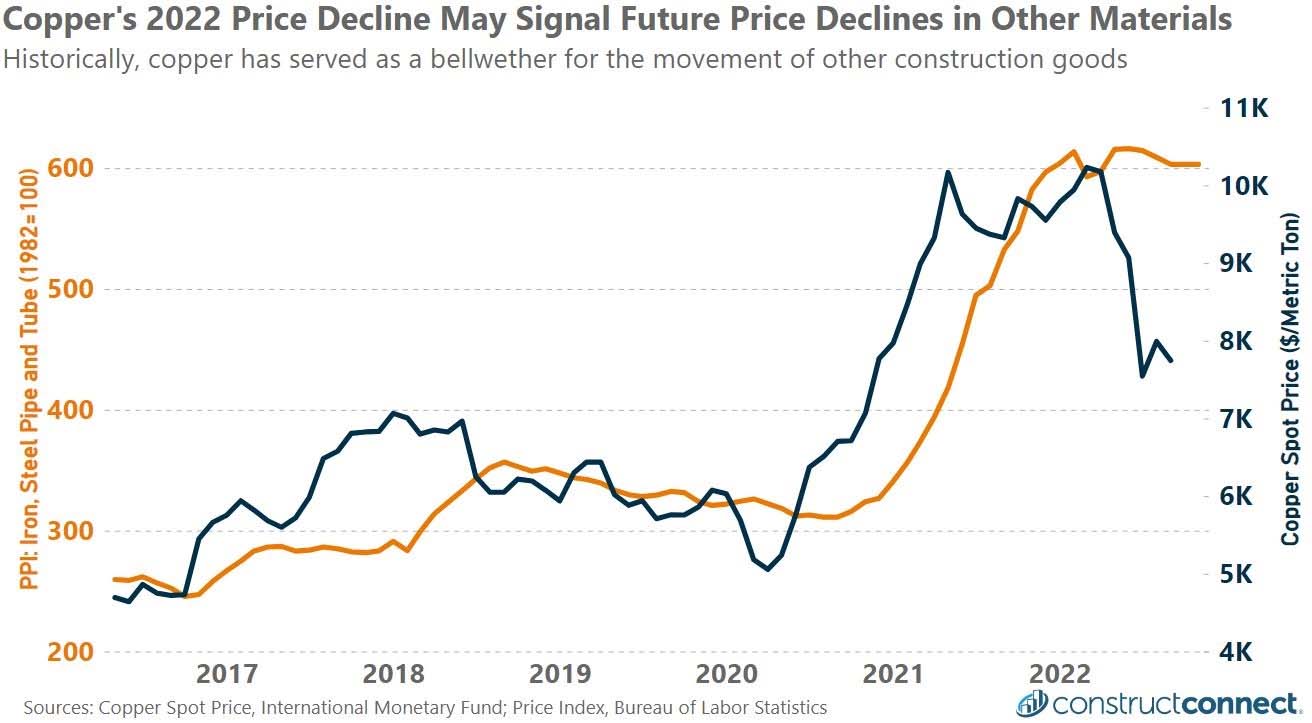

As such, a potential recession in 2023 coupled with high levels of supplier competition could result in declining inventory material prices after two years of strong price gains (see Figure 3).

COVID-19-driven desperation for supplies was evident in inventory-to-supply figures, which fell to a decade low in late 2020. However, decreasing demand for durable goods in 2022 and improving supply chain conditions have pushed this balance back not to their historical average, but rather to cyclical highs.

The industry’s latest challenge moving into 2023 is likely to be one of too much inventory. This will require taking a significantly different approach to operations and necessitate a change in inventory strategy that emphasizes price and less concern over future availability (see Figure 4).

Other Market Considerations

The monitoring of gross domestic product (GDP) alone is insufficient for the construction and distribution business leader. The latest available reading of quarterly GDP as of press time at 2.6% was met with elation by Wall Street and TV personalities.

However, this top-line number was exaggerated by inflation, which masked the economy’s true growth rate. Furthermore, the figure hid the stark contrast between a faster-growing services sector and a struggling durable goods sector. Adjusted for inflation, the durable goods sector barely grew at all in the 12-month period ending September 2022.

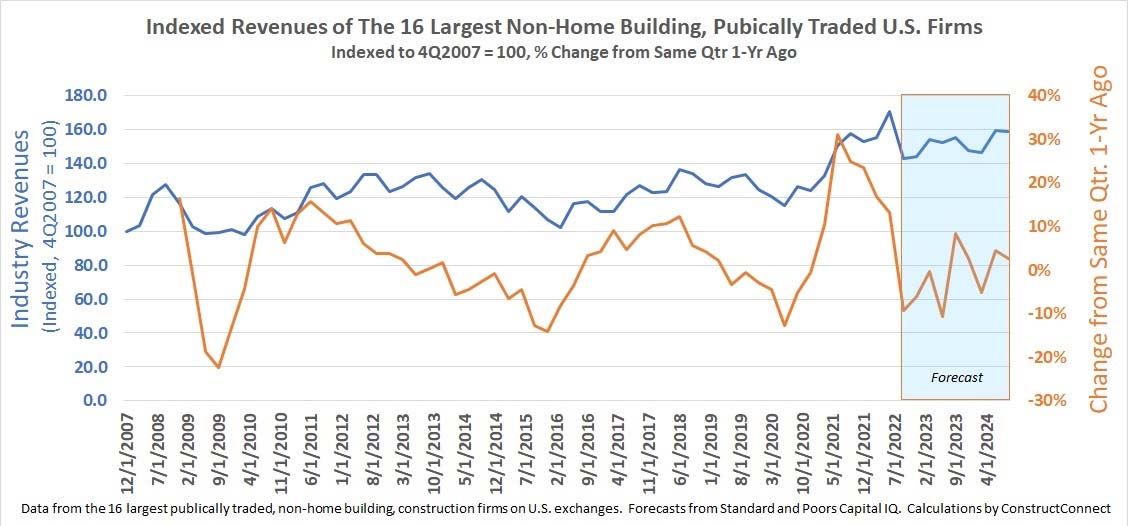

Wall Street’s outlook for the nonresidential construction market in 2023 and 2024 is significantly less sanguine than for the overall economy, with revenues for the 16 largest publicly traded nonresidential construction firms expected to fall 5% in 2023 before rebounding to low single-digit growth in 2024 (see Figure 5).

Lastly, the challenges facing the labor market need to be understood as a structural and long-term issue. COVID-19 drove a downward step change in the percentage of the baby-boomer generation in the labor force. As a nontrivial portion of them permanently left the labor force, they not only reduced the overall labor force’s size, but took with them their institutional knowledge and decades of experience.

In addition, it has been estimated that between 500,000 and 1 million workers of all ages left the workforce as a result of long-lasting COVID-19 symptoms. The absence of these seasoned workers has certainly further driven down the availability of skilled workers and is why the average productivity per worker in 2022 fell through at least the first three quarters of 2022, its longest and largest decline since before the Great Recession of 2008.

The consequence of a long-lasting, persistent labor shortage across the economy should encourage industry leaders to focus on how to do more with less labor. Product designers will need to design easy and quick-to-install products; architects will need to find ways to use less labor in the construction of their designs.

Furthermore, tradespeople will need to consider using tools and products that speed work or are faster to install. Making products that are more plug-and-play ready and require less experience to use and install will become a more important factor for the skilled trades industries moving forward.

Looking Ahead

The unique challenges the industry can expect to combat in 2023 and beyond will be substantially different from the challenges in the years following the COVID-19 pandemic. Rising market competition will make sales tougher while access to, and the cost of, inventories ease. Keeping excessive inventories will transition from serving as a safety net in recent times to a liability.

The ability to find, retain and train talent will continue to be significant issues for the industry as well as the greater economy. For wholesalers and tradespeople, this will encourage the marketing and adoption of labor-saving products that can be installed quickly and reliably by less experienced workers.

Finally, the rising likelihood of a cyclical downturn in 2023 naturally raises the question of its duration and amplitude. When gauging the entire economy, which includes both the goods and services sectors, the latest monthly survey data from the Wall Street Journal pointed to more than 60% of its surveyed economists expecting a very mild recession of only a few tenths of a percent through the first half of the year.

However, the fortunes of any individual industry can and often do vary greatly from broad economy expectations. This is where the individual or aggregated outlook of specific industry-leading firms can be very helpful and I would recall the aggregated outlook for the largest publicly traded construction firms in North America.

Although this outlook is not ideal, it is still possible to successfully navigate through this period by working smarter and not simply harder. Using the best and latest available data about the contours of the economy’s landscape can help firms redirect and or concentrate their efforts toward serving those parts of the economy that are expected to be least effected — if at all — by a downturn.

Looking at markets by vertical and market specifics can help firms to find pockets of opportunity, even when overall conditions are challenging.

Michael Guckes, Sr. Economist at ContstructConnect, has more than 20 years of economics experience, including eight years in civil construction and six years in manufacturing. Guckes joined ConstructConnect in 2022 to further strengthen their global leadership in construction economics and forecasting.