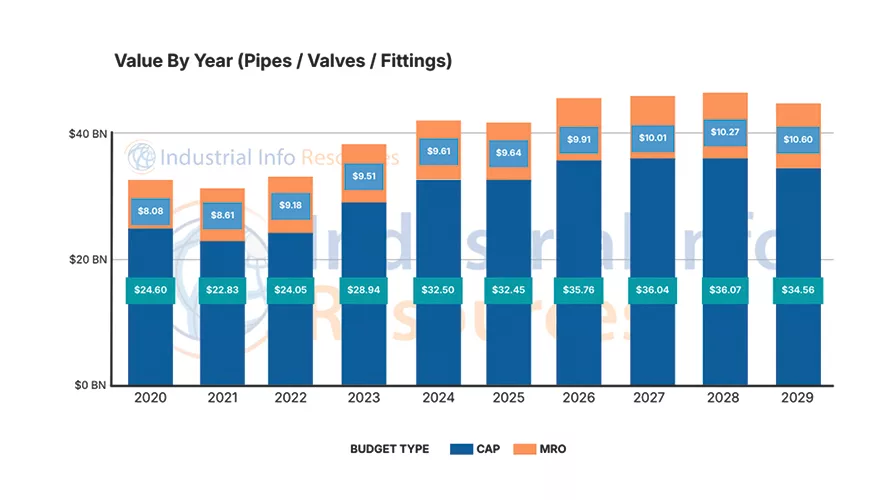

The value of pipe, valves and fittings (PVF) components in U.S. and Canadian industrial projects is forecast to jump 8.3% from $42.1 billion in 2025 to more than $45.6 billion this year, according to the latest available IIR PVF Forecast Analyzer. The forecast for 2026 includes $35.7 billion in PVF spending for capital projects and $9.9 billion for maintenance, repair and operations.

IIR’s PVF market forecast enables end-users to identify the size, location and timing of spending on a range of products across multiple industry sectors and geographies. The forecasts estimate spending related to capital investments and maintenance projects. The forecasts are based on a combination of projects being tracked globally, which are all updated daily, and IIR’s proprietary factoring methodology. This provides end-users with a unique bottom-up assessment of the current, five-year future and five-year historical demand and spending for a given range of industrial equipment and services.

The forecast includes:

1. Pipe. Aggregate spending covering cast iron, carbon and stainless steel, and plastic pipe.

2. Valves. Aggregate spending covering taps, angle and bib cocks, safety and relief valves, controls, regulators, gate, globe, plug, ball and butterfly valves, ballcock mechanisms and hand-operated valves.

3. Fittings. Fittings and elbows.

IIR’s current forecast extends to 2029, when the value of PVF components in American and Canadian projects is projected to reach $45 billion, a slight drop from the forecast for 2028.

For 2026, the oil and gas pipelines and chemical processing industries lead almost neck and neck in PVF spending, followed by metals and minerals and power. In all, IIR tracks 12 industries.

Oil and gas pipelines

IIR is tracking more than 300 capital pipeline projects in the U.S. and Canada with PVF components, planned to begin construction in 2026. In prior years, most of these projects were concentrated in the U.S. Southwest and western Canada, but the coming years could see development in other parts of the United States.

Investment in natural gas pipelines is expected to dominate the mix of pipeline projects in the coming years. Demand for natural gas is anticipated to continue to increase both domestically and internationally.

One growing driver of domestic demand is the power-hungry data centers being built across the country. Currently, data centers account for approximately 3% to 4% of total U.S. power demand. Some estimates indicate that demand could rise to 11% to 12% by 2030.

The natural gas pipeline sector will remain strong in the near term, with projects expected to be more prevalent in different regions than in previous years.

Demand for liquefied natural gas will remain a strong driver of natural gas pipeline development along the Gulf Coast and in western Canada.

Chemical processing

Over the last few years, the energy transition has been a prominent driver of major investments in the chemical processing industry as plant owners worked to meet their stated environmental and sustainability goals. These goals included reducing carbon dioxide (CO2) emissions and capturing CO2 from existing and proposed unit additions.

However, many of the planned projects had overly optimistic timelines. Numerous projects were stuck in limbo as plant owners tried to navigate the strict guidelines to qualify for stimulus incentives.

The passage of the One Big Beautiful Bill Act in 2025 impacted some of the government incentives driving many of the environmental, social and governance-motivated projects. This has led to many projects being delayed or cancelled altogether.

U.S. petrochemical market growth slowed in 2025 amid oversupply in the global market for many building block commodities, such as polyolefins. While the long-term view remains opportunistic, only a slight increase in the number of petrochemical and olefins projects is planned to begin construction in 2026.

Metals and minerals

The United States is advancing critical mineral projects for copper, lithium, cobalt and rare earths — essential for energy storage, electric vehicles and renewable technologies.

This includes supporting mining and downstream refining of critical minerals through partnerships, equity buy-ins, funding/grants and permitting programs. For example, in an effort to reduce the lengthy and costly permitting and regulatory process for new mines, the Trump administration has added 48 mining projects to the Fast 41 permitting program, which had only one project on the list a year ago.

However, recent policy shifts have also put several planned expansions and upgrades in jeopardy. The U.S. Department of Energy canceled more than $1 billion in grants in May designated for major carbon-capture projects at cement manufacturing facilities. Many companies remain committed, indicating that projects are only delayed.

Energy transition and green infrastructure programs are driving steel projects. Hyundai Steel’s $6 billion, 2.7 million-ton-per-year low-carbon steel plant in Donaldsonville, Louisiana, will be the first integrated electric arc furnace mill in the country targeting a 70% reduction in emissions versus traditional blast furnaces. The plant will provide metal for auto factories in Alabama and Georgia.

Canada is increasing efforts to strengthen domestic critical mineral supply chains and reduce reliance on foreign sources, particularly China. Government initiatives support exploration and mining of copper, nickel, lithium, gold, uranium and potash.

Our neighbor to the north is also fast-tracking the permitting process for major infrastructure projects and has created what it calls the Major Projects Office, which now includes six projects, including two mining projects. Smelters and rolling mills in Ontario and Quebec are investing in automation, renewable integration and recycling to reduce air emissions and boost resilience.

Power

The reversal of past U.S. administrations’ programs and initiatives, coupled with increased energy demand, new policies, legislation, a flurry of executive orders, tariffs, inflation and supply chain issues, continues to reshape the U.S. power industry.

Over the past year, IIR has seen a steady expansion of renewable energy projects, primarily solar and wind, a trend IIR believes will continue into 2026. However, with the passage of the One Big Beautiful Bill Act, the cutoff dates to obtain incentives and tax credits for these projects were shortened, leading to significant shifts in the development makeup for 2026. The acceleration of some projects to meet new production tax credit guidelines, as well as new energy demand levels, will be a driver in the solar market.

On the other hand, projects are being delayed by the same tax credit guidelines, permitting constraints — especially on federally owned land — and interconnect queue issues, as well as impacts from tariffs on foreign-made components.

In the fossil-fuel sector, significant changes have occurred in the composition of the natural gas and coal markets. Announcements of more spending in the natural gas-fired sector increased substantially in 2025, and this is expected to continue. Calls for natural gas-fired projects to be fast-tracked by the independent system operators, as well as partnerships between data center owners and utilities, and merchant power producers for outside and behind-the-meter generation development, have been a significant factor in shaping the market.

However, with increased development come both challenges and advantages. Heavy industrial gas turbine reservations and orders have placed the availability of larger turbines at least 36 months out, prompting developers to turn to smaller gas turbines and internal combustion engines to meet electricity demand.

Examining the operational fleet, spending over the last couple of years in the natural gas market has focused on maintenance activities and an increased push to modify existing gas turbines to enhance efficiency and increase power output.

IIR will continue to see retirements in the coal-fired generation fleet, but this sector is seeing changes. Executive orders, as well as the call for base-load sustainable power, have increased the number of announcements of retirement delays; this trend is likely to continue this year. Consequently, an increase in fleet maintenance is also occurring.

The rollback of environmental mandates implemented by the prior administration and the defunding of the Department of Energy’s emissions-reduction initiative have also impacted development and spending.

The nuclear sector is also seeing many changes. These include executive orders promoting changes to the Nuclear Regulatory Commission’s permitting and licensing of projects, as well as the review timeframes surrounding new technology.

Plans to restart retired or previously closed nuclear power generation facilities are expected to continue into 2026. One of the major drivers of this is on-site power demands from industrial sectors such as data centers.

The transmission and distribution side of the industry continues to grow, with substantial development announcements and construction starts to continue into 2026. The spending is intended to support renewable energy development and meet growing energy demand.

Examining the Canadian power market reveals several notable similarities with the U.S. market — the continued development of renewable energy, further development of nuclear generation and increased spending.

Brian Ford is editor in chief at Industrial Info Resources and has been with IIR since 2014. With global headquarters in Sugar Land, Texas, and 18 offices worldwide, IIR is a provider of global market intelligence specializing in the industrial process, heavy manufacturing and energy markets. To contact IIR, visit www.industrialinfo.com or call 713-783-5147.